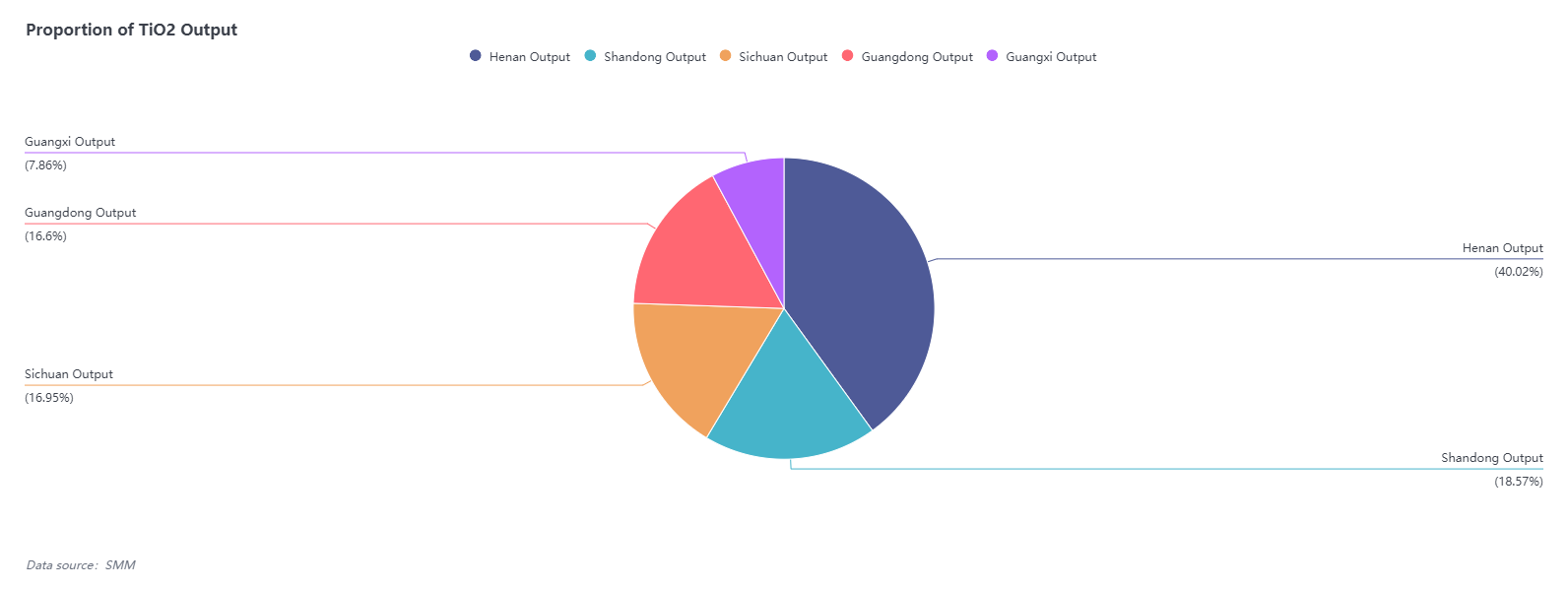

1 Titanium Dioxide

1.1 Prices Bottomed Out and Rebounded

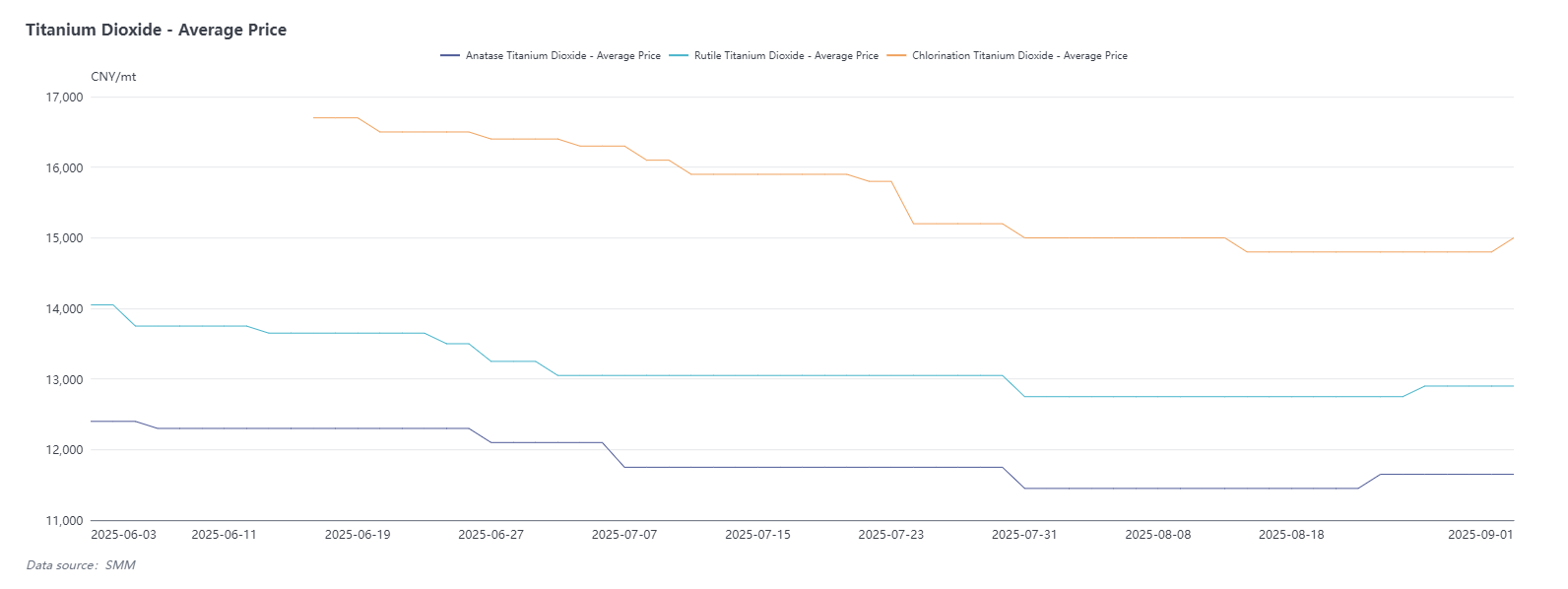

As of the latest update, anatase titanium dioxide is quoted at RMB 11,500-11,800/mt (avg. RMB 11,650/mt); rutile titanium dioxide is quoted at RMB 12,600-13,200/mt, with FOB offers at USD 1,825-1,875/mt; chloride-process titanium dioxide is domestically quoted at RMB 14,500-15,500/mt, with FOB offers at USD 2,040-2,140/mt.

In August, the titanium dioxide market gradually recovered after a period of low consolidation. Price cuts by some producers in late July led to new lows in early August, with chloride-process titanium dioxide continuing to decline due to inventory buildup, while the price gap between tier-1, tier-2, and tier-3 rutile producers narrowed significantly, intensifying market competition. By mid-August, multiple companies issued price adjustment notices: domestic prices generally increased by about RMB 500/mt, while export prices rose by approximately USD 70/mt. Although most August orders had already been signed when the notices were issued, and downstream market reaction was initially muted due to lack of rigid demand, anatase titanium dioxide led the gains in late August, with transaction prices rising by about RMB 200/mt. Rutile transaction prices followed with an increase of about RMB 250/mt. Recently, domestic chloride-process prices increased by RMB 200/mt, while international prices remained stable. Future price trends will depend on the release of actual procurement demand in September.

1.2 Titanium Dioxide Production and Inventory Both Decline, Market Downturn Stabilizes

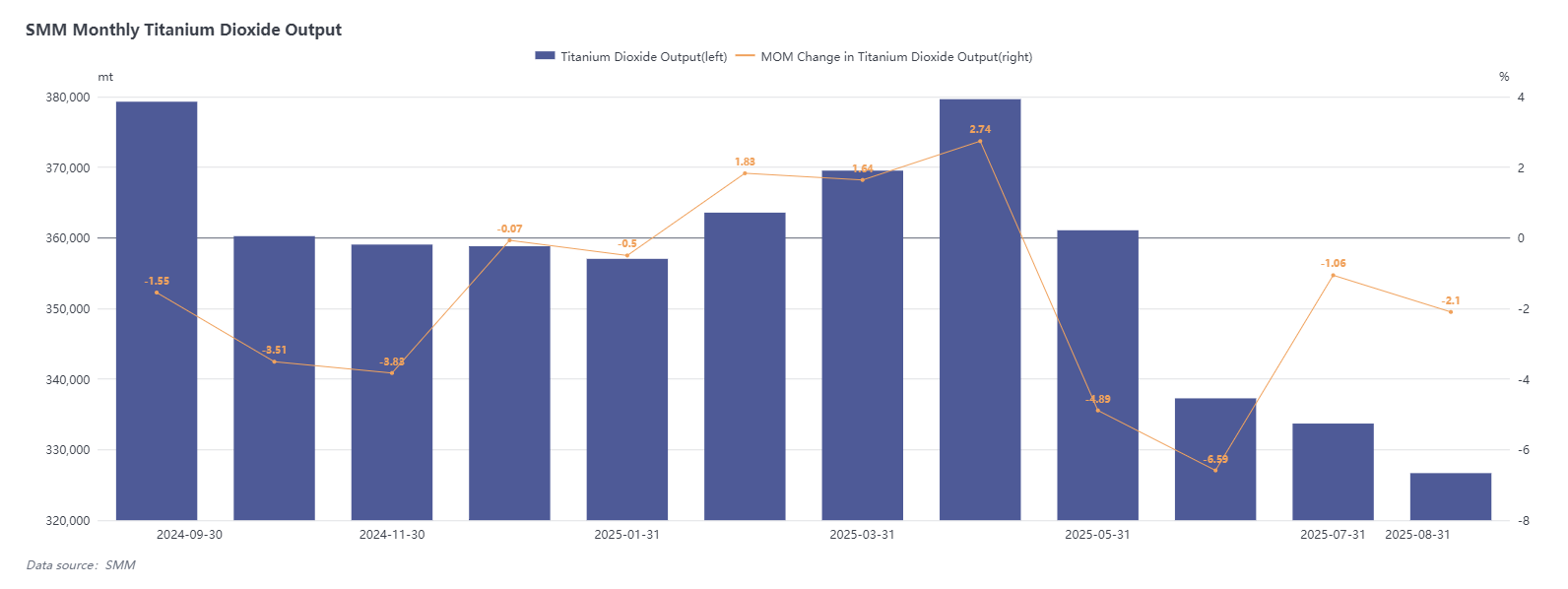

According to SMM data, national titanium dioxide production in August was approximately 326.7k mt, down 2.1% month-on-month (MoM); inventory was about 388.8k mt, down 1.21% MoM. Small producers continued production cuts, with output further contracting, while some idled companies actively reduced inventories. The earlier production cuts are now showing results, with producer inventories effectively digested, coupled with steadily recovering downstream demand. The previous downward trend in the titanium dioxide market has largely halted. With continued demand support in September, supply is expected to remain tight, potentially driving further price increases.

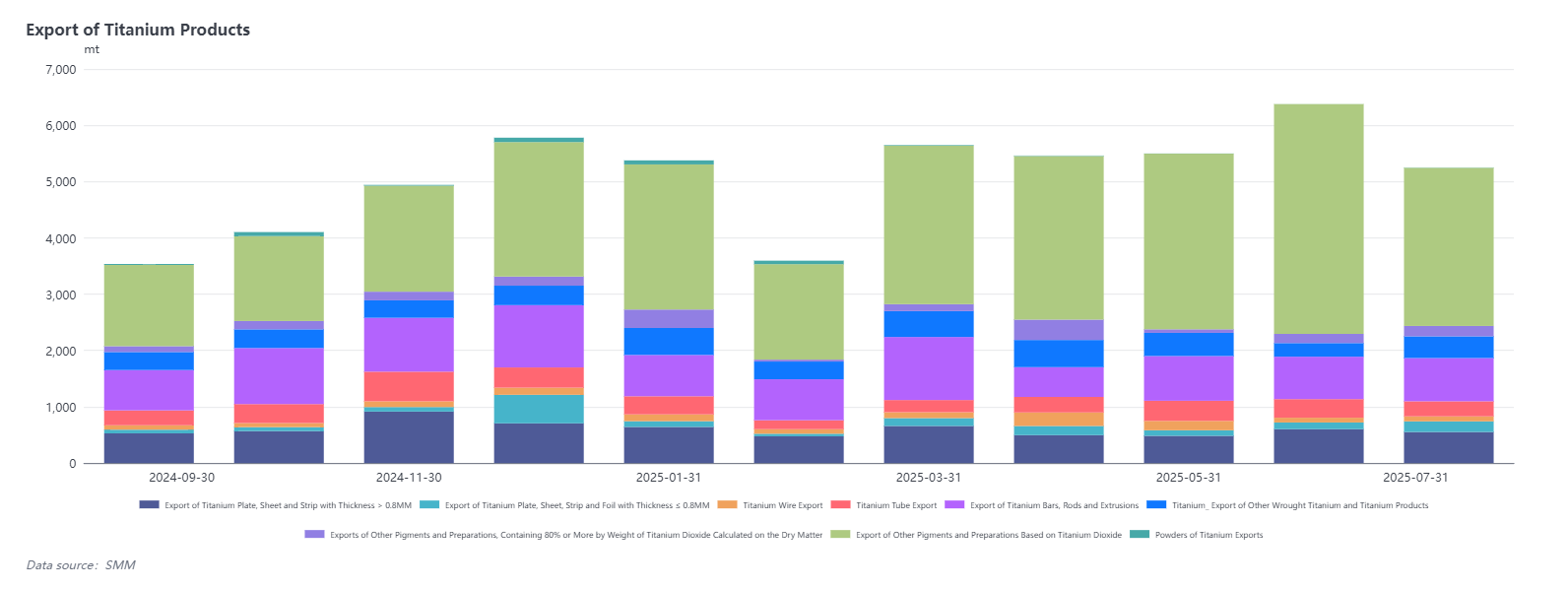

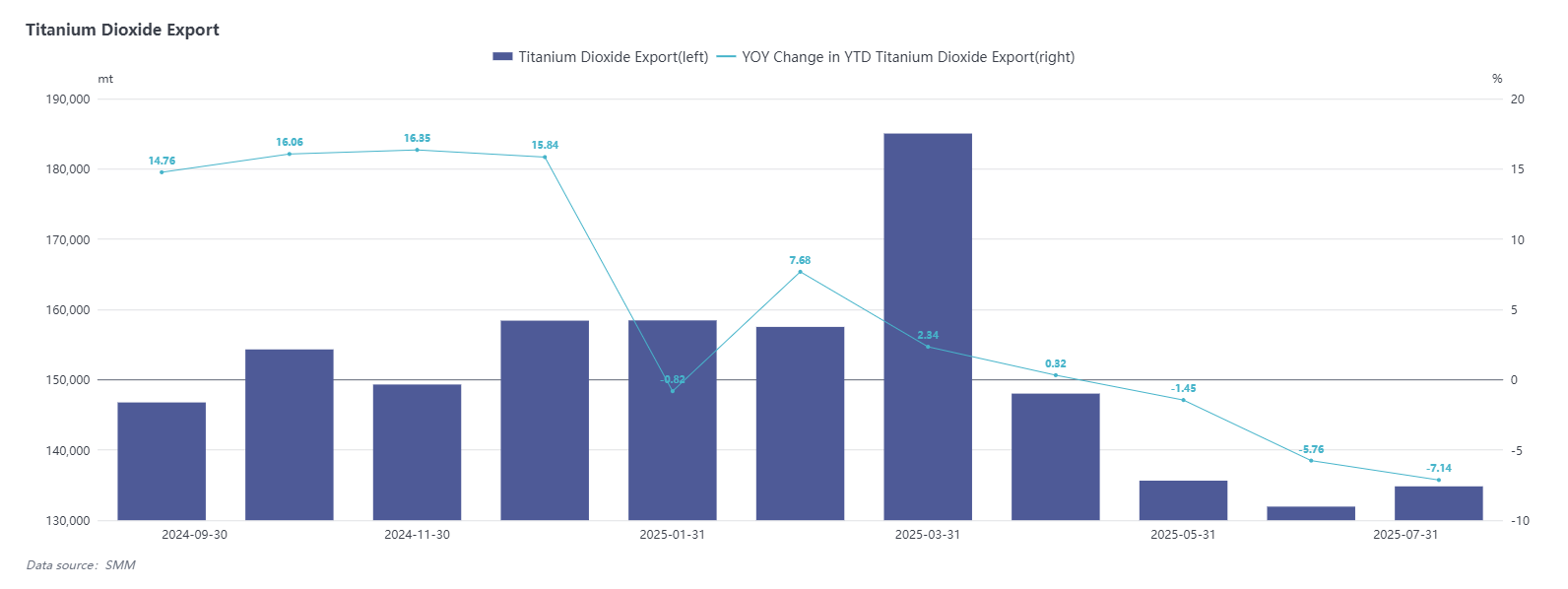

1.3 Titanium Dioxide Exports Decline Year-on-Year, Multiple Factors Keep August Pressure

Latest customs data shows a significant decline in titanium dioxide exports since May. July exports increased 2.19% MoM to 135k mt but decreased 7.14% year-on-year (YoY). The export weakness is mainly due to three factors: significant contraction in overseas demand, intensified international competition leading to sustained pressure on export prices; increased pressure in key export regions and narrowing profit margins due to "anti-dumping" policies in multiple countries; and domestic production cuts and shutdowns in July, which objectively limited export supply. The weak export trend is expected to continue in August, with a slight recovery anticipated in September driven by the traditional peak season.

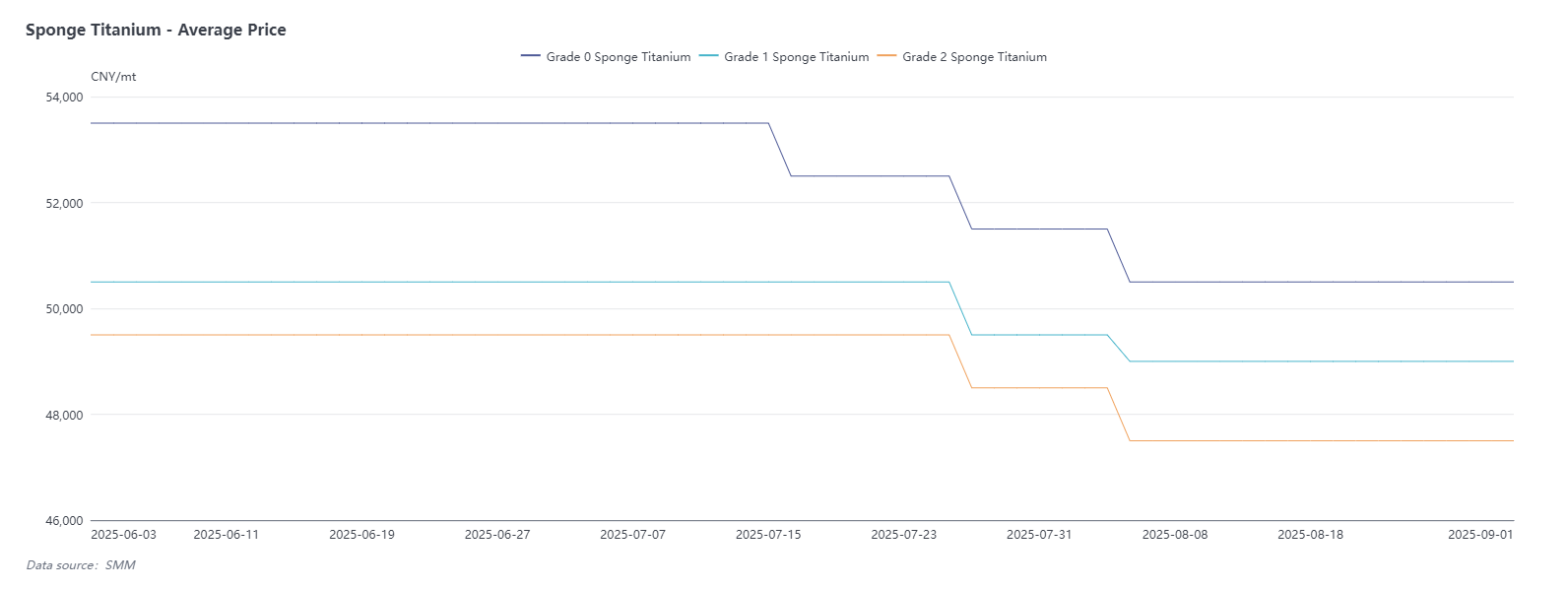

2 Sponge Titanium

2.1 Sponge Titanium Prices Stabilized After Early August Decline, Production Cuts Provide Support but Demand Needs Boost

As of the latest update, grade-0 sponge titanium is quoted at RMB 50,000-51,000/mt (avg. RMB 50,500/mt); grade-1 sponge titanium is quoted at RMB 48,000-50,000/mt (avg. RMB 49,000/mt).

In August, sponge titanium prices consolidated at low levels after a slight decline early in the month. Weak demand from the titanium materials market led to subdued transactions. However, production cut plans announced by major producers in mid-August tightened supply expectations and gradually restored market confidence. Although inventories remain high, price declines have been effectively curbed under production control measures, and the market has entered a phase of horizontal consolidation. Future price trends will depend heavily on the recovery of demand in the titanium materials market.

2.2 August Sponge Titanium Production Cuts Show Effect, Output Decline Unlikely to Change Low Price Trend in September

According to SMM data, sponge titanium production in August was 20.9k mt, down 9.39% MoM. The market actively responded to "anti-involution" policies by announcing production cuts, with planned reductions of up to 30% to actively control capacity. Another key reason is that after significant capacity expansion earlier, downstream demand has been unable to absorb the excess supply, pushing prices into a downward trend. SMM surveys indicate that actual production cuts were slightly lower than announced plans, mainly due to the complexity of cost-related adjustments and the time needed for full implementation. However, the decline in sponge titanium prices has gradually moderated. Based on current market conditions, prices are expected to remain low in September.

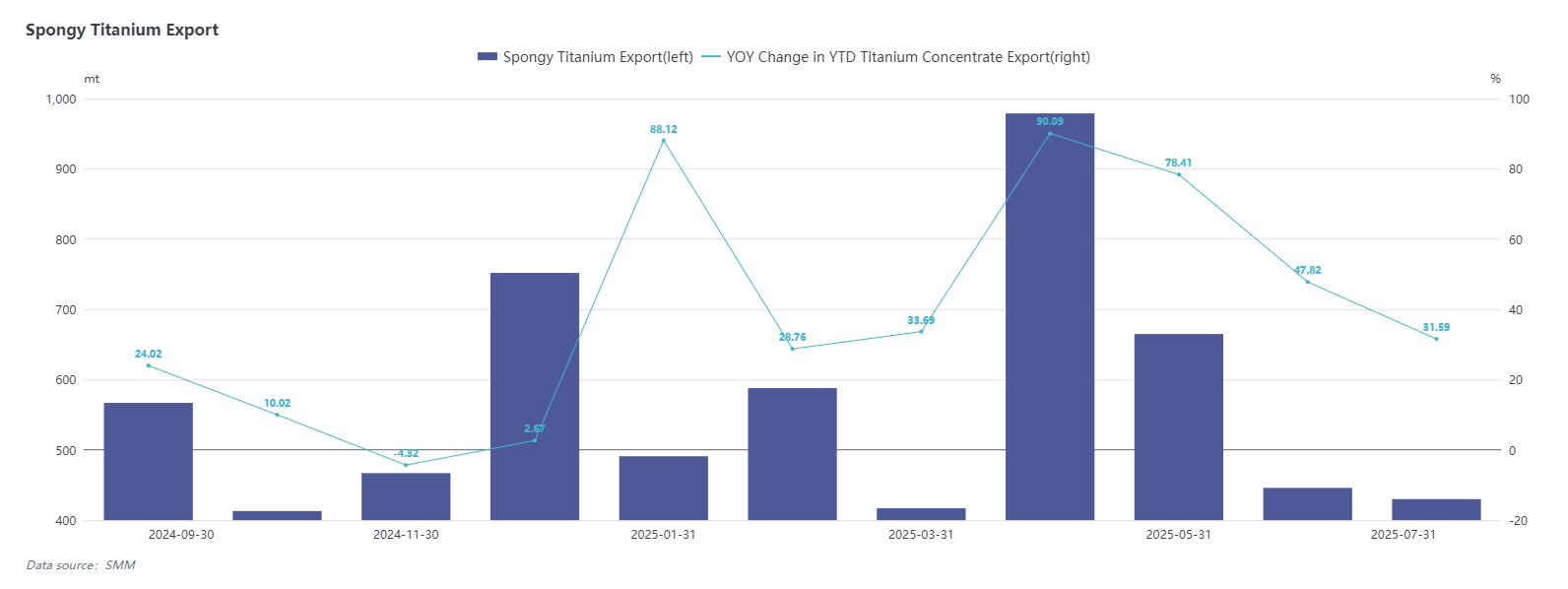

2.3 Sponge Titanium Exports Limited but Show Strong YoY Growth, Seasonal Peak Expected to Drive Demand Recovery

Latest customs data shows sponge titanium exports fell to 430 mt in July, down 3.59% MoM, but cumulative exports still increased 31.59% YoY, though the overall export scale remains limited. Titanium materials exports were about 5.2k mt, slightly lower than June. The export weakness was mainly due to the summer holiday period overseas, with seasonal demand contraction intensifying competition and weakening performance. However, cumulative YoY data indicates a significant increase in direct demand for sponge titanium this year. Exports are expected to rebound in September with the traditional peak season.